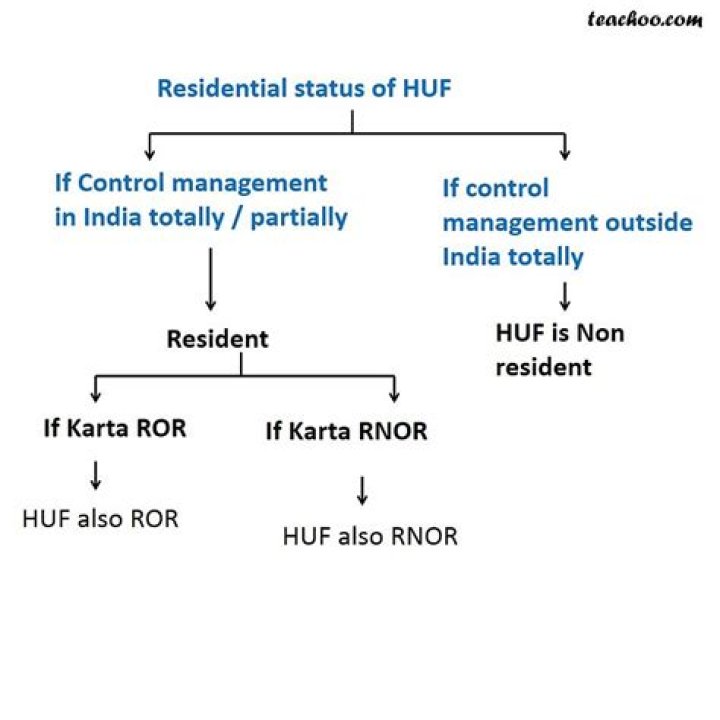

A Hindu undivided family is a non-resident in India if the control and management of its affairs is wholly situated out of India. In order to determine whether a Hindu Undivided Family is a resident or a non-resident, the residential status of the karta of the family during the previous year is not relevant. Subsequently, one may also ask, how do you determine the residential status of HUF?

Residential Status of HUF

A Hindu Undivided Family (HUF) is said to be resident in India if the control and management of its affairs are wholly or partly situated in India. (ii) he has been in India for a period of 730 days or more during 7 years immediately preceding the relevant year.

Subsequently, question is, what are the 2 conditions for claiming HUF status? The HUF shall be said to be resident and ordinarily resident in India if the karta of the HUF satisfies both the following conditions: He (Karta) must be resident in at least 2 out of 10 previous years immediately preceding the relevant previous year; and.

Considering this, how do you determine the residential status of a company?

- With effect from Assessment Year 2017-18, a company is said to be resident in India in any previous year, if:

- (i) it is an Indian company; or.

- (ii) its place of effective management, at any time in that year, is in India.

What is the residential status of an Indian company?

An Indian company is always resident in India. Even if an Indian company is controlled from a place located outside India (or even if shareholders of an Indian company controlling more than 51 per cent voting power are non-resident and/or located outside India), the Indian company is resident in India.

Related Question Answers

What is our residential status?

Residential status is a term coined under Income Tax Act and has nothing to do with nationality or domicile of a person. Residential status of a person depends upon the territorial connections of the person with this country, i.e., for how many days he has physically stayed in India. What is the purpose behind determination of residential status?

Determination of the residential status is one of the basic and important aspects to determine the nature and the scope of the income of the persons which comes under the tax net. The residential status of person can be broadly be classified into three categories such as Resident, Non Resident and Deemed Resident. Which section is related to residential status?

Section 6 of the Income-tax Act, 1961 (the Act) contains provisions relating to residency of a person. The status of an individual as to whether he is resident in India or a non-resident or not ordinarily resident, is dependent, inter-alia, on the period for which the person is in India during a year. Can Huf be NRI?

A HUF can also be a non resident HUF if all the members of the family are non residents, as per the common understanding of the term non resident. The person in charge of the HUF is called a Karta or manager. So, NRO account can be opened for HUF. This is confirmed by RBI in the Master Circular for NRO accounts. When a company is a resident?

Residential Status of Companies under the Income tax Act, 1961: Section 6(3) of the Income tax Act, 1961 provides that a Company is said to be resident in India in any previous year if: The Company is an Indian Resident; OR. Its place of effective management, in that year, is in India. What are the conditions for determining residential status of an individual?

She said, "The residential status is determined based on the number of days of physical presence of the taxpayer in India (irrespective of the purpose of stay) during the financial year and preceding ten financial years. What is non resident company?

A company would be considered non-resident if the control and management is not in India. The location of board of directors should determine the place of control and management of the company. MUMBAI: A company would be considered non-resident if the control and management is not in India. When can Huf be formed?

An HUF is automatically constituted after marriage. It can also be formed by partition of an existing HUF into multiple units. An HUF is automatically constituted after marriage. It can also be formed by partition of an existing HUF into multiple units. Who is a resident under Income Tax Act?

A resident taxpayer is an individual who satisfies one of the following conditions: Resides in India for a minimum of 182 days in a year. Has resided in India for a minimum of 365 days in the immediately preceding four years. In addition, he must reside in India for a minimum of 60 days in the current financial year. What is assessment year?

The assessment year (AY) is the year that comes after the FY. This is the time in which the income earned during FY is assessed and taxed. Both FY and AY start on 1 April and end on 31 March. For instance, FY 2019-20 and AY 2020-21 are one and the same. What do you mean by resident company?

A company is said to be resident in India in any previous year. It is an Indian Company ; or. during the relevant previous year the control and management of its affairs is situated wholly in India. Which allowances and requisites are totally exempted?

The benefits received by a salaried employee over and above their wages or salary are termed as perquisites. Depending on the nature, perquisites can be taxable or non-taxable. Uniform allowance is an example of perquisite and is exempt up to the limit as described under section 10(14) of Income Tax Act. Can one person be Karta of 2 HUF?

It is possible a person can be Karta in two HUF. 13 June 2013 Yes you can have two HUFs. One your father's HUF and secondly your HUF. Till your father's HUF is partioned yu can continue to be be the karta of the said HUF if you are the eldest son otherwise the eldest son shall be the karta. Can Huf be formed without a child?

HUF can be created even if there is daughter (female child). He can have his own huf in that case without any child ( he and his wife being the members of HUF). 2) Yes he can have his own huf created and be a Karta. Simultaneously he can remain a member of bigger HUF i.e his father's HUF. Can female be a Karta?

Now that this disqualification has been removed by the Hindu Succession (Amendment) Act, 2005, there is no reason why Hindu women should be denied the position of a Karta. If a male member of an HUF, by virtue of his being the first born eldest, can be a Karta, so can a female member. Can wife be Karta of HUF?

Can a Woman be HUF Karta? Yes! Until January 2016, a woman could not be the HUF Karta. But in a landmark case, the Delhi High Court ruled in favour of a female being the Karta of a HUF. Is daughter in law member of HUF?

After marriage, daughter ceases to be a member of father's HUF but still, she is a coparcener. If the daughter dies intestate, her share in the HUF property passes by succession to her legal heirs as per section 15 of the 1956 Act. A daughter is a coparcener but a daughter in-law is only a member of joint family. How is HUF property divided?

Under Hindu Law once the status of Hindu Family is put to an end, there is notional division of properties among the members and the joint ownership of property comes to an end. In total partition all the members cease to be members of the HUF and all the properties cease to be properties belonging to the said HUF. Can Karta withdraw money from HUF?

yes karta can withdraw the money. But the other coparners can obtain court injunction provided that they can substantiate that the karta wants to convert HUF property to his personal property. What happens if Karta of HUF dies?

One the death of a karta, the next senior most member automatically becomes the new karta of the HUF but at times, statutory authorities may require a declaration from the members forming part of the HUF declaring the eldest coparcener as the new karta of the HUF. Can HUF do any business?

Since HUF is one person as per Income Tax Act, a Proprietor of a business can be an Individual or a HUF. A Proprietorship concern is not governed by any specific law as such, and therefore there is no bar on HUF becoming a Proprietor of any concern. Do NRI pay tax in India?

If your status is 'NRI,' your income which is earned or accrued in India is taxable in India. Income which is earned outside India is not taxable in India. Interest earned on an NRE account and FCNR account is tax-free. Interest on NRO account is taxable for an NRI. Is stock dividend taxable in India?

Answer: In India, a company which has declared, distributed or paid any amount as a dividend, is required to pay a dividend distribution tax at 15%. Only a domestic company is liable for the tax. Domestic companies have to pay the tax even if the company is not liable to pay any tax on their income. Can a company not ordinarily resident in India?

As per the current tax laws, an individual would qualify as a 'not-ordinarily resident' if he has been a 'Non-Resident' in India in at-least nine out of the ten previous tax years or has been in India for an overall period of 729 days or less during the seven previous tax years. What is scope of total income?

Scope of total income. Scope of total income. 5. ( 1) Subject to the provisions of this Act, the total income of any previous year of a person who is a resident includes all income from whatever source derived which— (a) is received or is deemed to be received in India in such year by or on behalf of such person ; or. What is the meaning of resident Indian?

To qualify as a resident Indian, an individual should have spent 182 days or more of a financial year in India, or stayed in India for 60 days or more in the year and for a period of 365 days or more in the 4 years preceding the relevant financial year. What is net annual value in income tax?

The Annual Value is determined after taking 4 factors into consideration. These are: (i) Actual rent received or receivable (ii) Municipal Value (iii) Fair Rent (iv) Standard rent. Net Annual Value is calculated as gross annual value less municipal taxes paid. CALCULATION OF INCOME FROM HOUSE PROPERTY. When an individual is considered a non resident in India?

As per Section 6 of the Income-tax Act, an individual is said to be non-resident in India if he is not a resident in India. 2. If he is in India for a period of 60 days or more during the previous year and 365 days or more during 4 years immediately preceding that year.